Special Report: State of the Industry

2017 State of the Industry Study

What are the latest trends in flexible packaging? Biggest challenges? Anticipated change in sales?

We wanted to know, so we partnered with BNP Media’s market research division in an effort to better understand the current state of the industry. The study focused on packaging and the perceived goals and challenges, with the objective of providing the industry with a better understanding of two other key factors:

- Sales trends and budget allocated to packaging.

- Equipment and product purchase plans for 2017.

The survey was distributed to 6,821 active, qualified Flexible Packaging subscribers from January 3-17. About one-third (32 percent) of all respondents indicated converting as their primary business, while 19 percent identified themselves as material suppliers. Contract packers/co-packers (10 percent), end user/brand owner/manufacturer (10 percent) and equipment suppliers (9 percent) were other notable respondents that rounded out the study.

In terms of 2016 budget allocations, respondents stated they spent the most on packaging materials (39 percent), followed by equipment/machinery (24 percent), design/print services (23 percent) and miscellaneous items (14 percent). In terms of packaging materials, more than half of all respondents stated that they use such for flexible packaging purposes.

Here’s a closer look at some of the key findings:

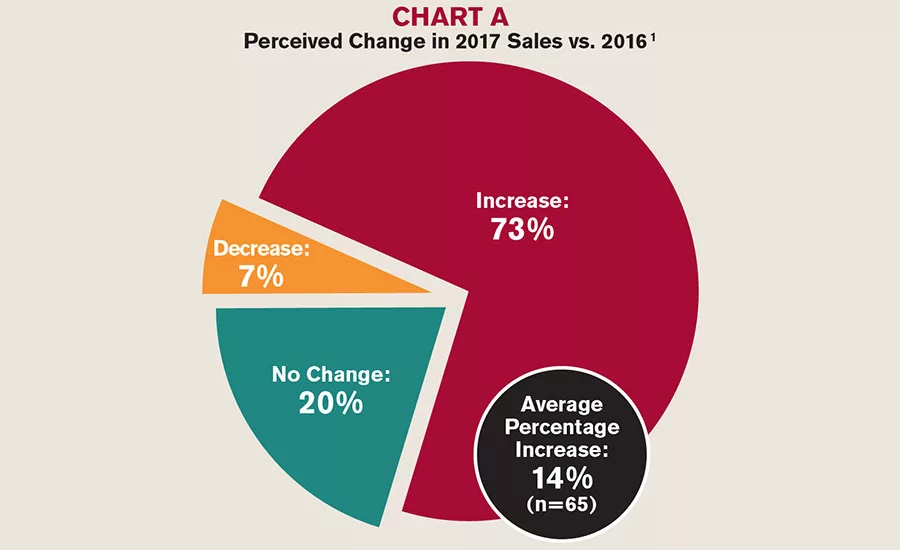

Anticipated Overall Sales Increase

Almost three-quarters of all respondents (73 percent) stated they expect an increase in their company’s overall sales in 2017 versus 2016. The average anticipated increase is 14 percent. Twenty percent of respondents stated they expect no change in sales and only 7 percent stated that a decrease is anticipated. See Chart A.

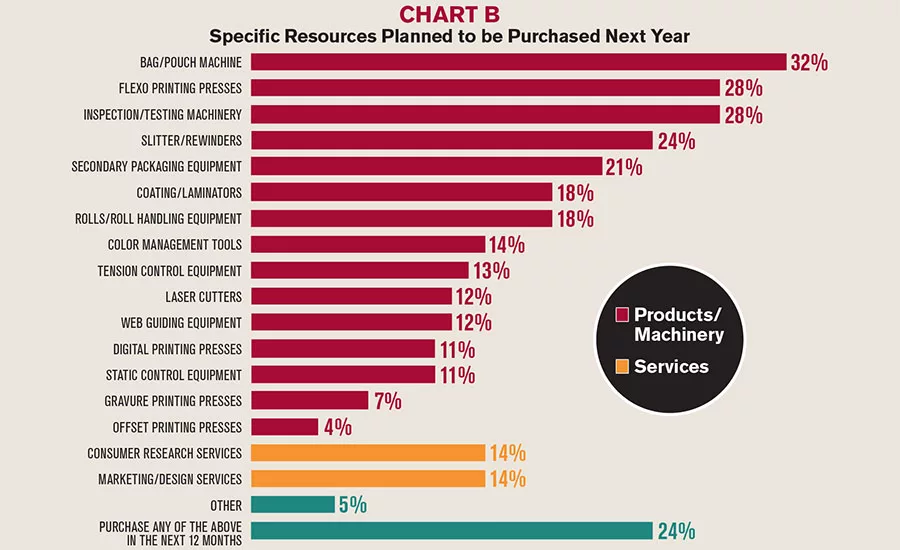

Resource Planning

The study indicated that overall resource investment across five categories – sales/marketing, equipment/machinery, materials, creative/design services and sustainability – is likely to remain similar in 2017 to what companies invested in 2016. However, respondents identified that they’re likely to invest more of their overall resources into equipment and product purchases, and sales and marketing.

What exactly are respondents likely to be investing in? Bag/pouch machinery tops the list at 32 percent, while flexo presses and inspection/testing equipment each come in at 28 percent. Slitter/rewinders (24 percent), secondary equipment (21 percent), coating/laminators (18 percent) and roll/roll handling equipment (18 percent) are other notable purchase categories. See Chart B.

Trends and Challenges

Not surprisingly, the top trends identified all fell in the broad category of sustainability. Within this category, respondents identified recyclability, environmental friendliness and bio-based materials as key trends. Pouches – specifically standup pouches and transparent pouches – were the next most commonly identified trend, followed by shorter runs/turnaround time, digital printing, lightweighting and downgauging.

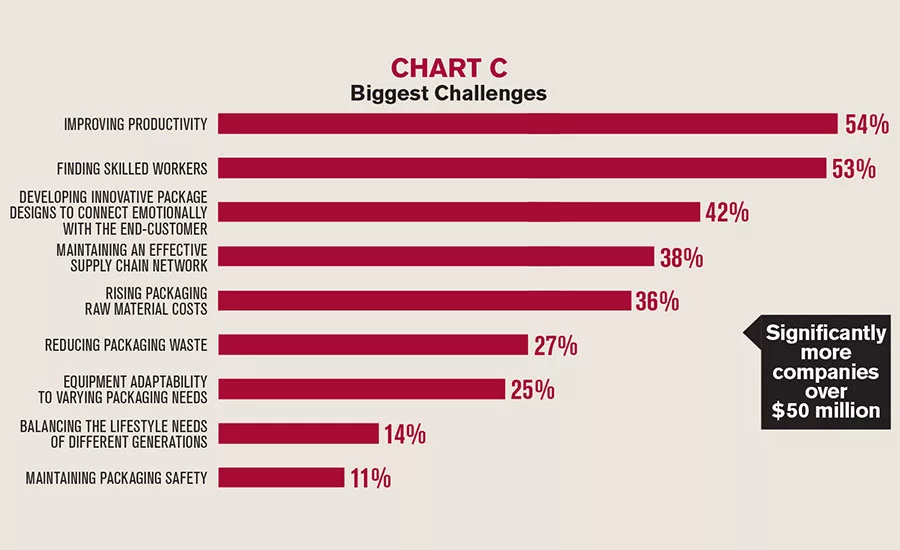

Companies aren’t without their challenges. At 54 percent, improving productivity was identified as the biggest challenge among survey respondents, with finding skilled workers (53 percent) coming in second. Developing innovative packaging (42 percent), maintaining an effective supply chain (38 percent), rising raw material costs (36 percent) and reducing packaging waste (27 percent) were other notable challenges that respondents identified. See Chart C.

Competitive Advantages and Initiatives

Another aspect of the study centered on where respondents believed they held a competitive advantage over others in the industry. Price and product innovation topped this list, with time-to-market, supply chain management, quality and flexibility rounding out other notable categories.

The study also aimed to get a better understanding of how companies are taking initiative moving forward. The majority of respondents stated that they’ve taken the initiative to continue operational performance improvement, further develop customer dialogue and to be more sustainable. In terms of sustainability, most respondents stated that they plan to use a lesser amount of materials or put a greater focus on worker safety and clean technology to meet such goals.

Outsourcing

About one-third of study respondents indicated that they outsource operations, with the most commonly outsourced task being manufacturing/processing.

A better ability to manage capacity needs was the most popular factor cited behind outsourcing, with increased flexibility, ability to meet customer demands and gaining better expertise as other top reasons.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!