FPA Update

FPA 2017 State of the Flexible Packaging Industry Report

Imports & Exports and Industry Challenges/Vision

The State of the Flexible Packaging Industry Report (SOI) is a definitive source of information regarding the flexible packaging industry size, structure, market segments, and key packaging products. Data in the Report is primarily based on research conducted by FPA, which includes surveys of FPA converter and material/equipment supplier members. Secondary data sourced from the U.S. Census Bureau, U.S. Department of Labor, U.S. Department of Commerce, industry analysts, and investment banking reports is also included within the Report. Several aspects of the industry are examined within the Report, including performance; materials and processes; end-uses; industry structure; imports and exports; and industry vision and challenges.

The 2017 Report provides an overview of the performance of the U.S. flexible packaging industry in 2016. The Report focuses on the value added segment of the U.S. flexible packaging industry, which enhances flexible materials by performing multiple processes such as extrusion, lamination, and printing.

FPA concludes its review of the 2017 Report within this issue of the FPA Update. This month, the “Imports & Exports” and “Industry Issues/Vision” sections of the Report are highlighted.

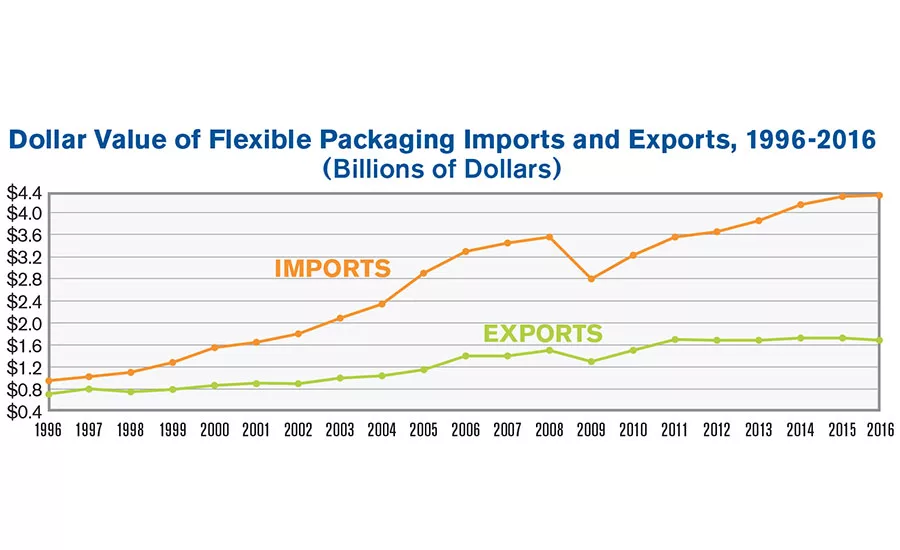

Imports & Exports

Flexible packaging exports have accounted for a relatively consistent share of domestic production (measured in dollars) over the past 10 years. U.S. flexible packaging exports were down slightly at $1,698 million in 2016 versus $1,721 million in 2015. Canada and Mexico remain the two largest purchasers of U.S. flexible packaging exports, followed by the United Kingdom. However, the U.S. flexible packaging industry’s trade deficit – the difference between exports and imports – increased moderately in 2016, rising 2.3% to the level of nearly $2.61 billion, compared with $2.55 billion in 2015. Additional U.S. flexible packaging import and export data is provided in the Appendix section of the 2017 SOI Report.

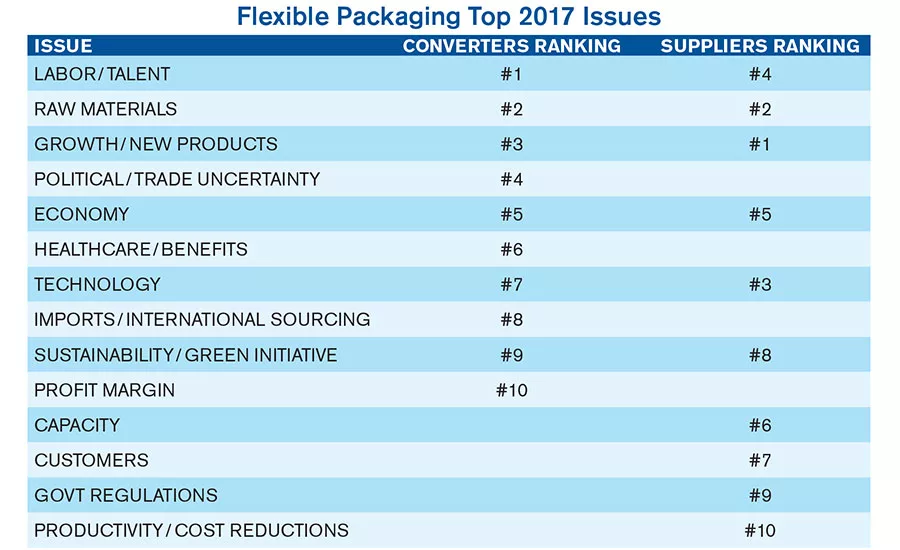

Industry Challenges/Vision

A comparison of the top challenges facing the flexible packaging industry for converters and suppliers indicates that labor/talent is the new top issue for converters (and one of the top five issues for suppliers), replacing raw materials. In an open ended survey question, FPA converter and supplier members were asked their vision of where the flexible packaging industry is headed over the next three to five years. The responses included: industry consolidation will continue; steady industry growth based on improvement in U.S./global economy; continued rigid to flexible conversion; and increased emphasis on consumer value as converters utilize technical improvements in aseptic, retort, shelf stable, anti-counterfeit, and child resistant packaging.

For More Information

For more information on the FPA 2017 State of the Flexible Packaging Industry Report, contact FPA’s Business & Economic Research Division, at fpa@flexpack.org or 410-694-0800, or visit www.flexpack.org.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!