Cover Story: Packaging Outlook

Packaging Outlook 2017

This report is an excerpt from the 2017 Packaging Outlook Report, featured in Packaging Strategies NEWS.

Within the layered approach to brand protection are overt – barcodes, holograms, watermarks, embossing and etching – and covert technologies – taggants, UV, infrared and fluorescent inks, smart technology and radio frequency identification (RFID).

Photo courtesy: DuPont

Folding Carton Packaging

In 2015, the last year for which complete figures are available, the North American industry shipped 4.94 million tons of paperboard packaging with an average value per ton of $1,765, according to the Paperboard Packaging Council (PPC). This is down from the 5.03 million tons shipped in 2014. The good news is that while the tonnage of paperboard shipped in 2015 was less than 2013, the value was higher. Some 5.02 million tons were shipped in 2013, with an average value per ton of $1,742.

The dollar value of shipments dropped to a four-year low for 2015. U.S. folding carton shipments totaled $8.71 billion in 2015, down from $8.94 in 2014, $8.76 in 2013 and $8.84 in 2012. In the five-year period between 2015-2019, the industry is expected to grow at an average annual rate of 1.3% in sales and 0.5% in tons. The average value per ton per year is expected to rise 0.8%, according to RISI.

Further reporting from RISI predicts that folding carton shipments will drop by 1.9% in 2016, once all the statistics are tallied. Despite the dip, RISI forecasts that folding carton shipments will increase at a 0.5% annual rate over the next five years. The shipment growth is expected to be healthier in the latter part of the forecast, improving steadily over the years, making it closer to 1% growth by the end of 2021.

The total value of U.S. carton shipments should climb from as estimated $8.7 billion in 2015 to $8.9 billion in 2019.

The PPC reports that increasing boxboard prices remain a strong hindrance to growth in the market. From 2010-2015, paperboard costs rose at an average rate of 2.8%; in comparison, the average values of folding cartons only increased by 1.7%. Naturally, this disparity between boxboard prices and folding carton values has cut into carton-makers’ profits. Europe, however, is reportedly ramping up boxboard tonnage, and the Chinese market is currently oversupplied. Those factors may work to decrease the problem as the increased capacity makes its way to the U.S. market.

Nothing has changed in the general breakdown of the industry. Independently owned, private companies (defined as converters who do not own their own mill, several of which are ranked in the top 10 by volume), comprise about 20% of industry sales. Market share has declined from approximately 30% over the past 15 years, due primarily to industry consolidation.

As always, the folding carton market must strive to differentiate itself from alternative packaging methods and materials, especially low-priced plastic. However, the industry’s much greater environmental profile should keep it strongly competitive.

Corrugated

The corrugated industry continues to struggle, regrouping from the huge decline in shipments it experienced nearly a decade ago. But the numbers have climbed slowly since 2009—a small, but welcome, sign of recovery.

According to statistics compiled by the Fibre Box Association (FBA), corrugated industry shipments totaled more than 368.6 billion sq ft in 2015, the last year for which final statistics are available, which is a slight increase of 1.2% over 2014 totals. Although growth remains a bit anemic, any signs of upward activity should still be viewed in a positive light, considering the rollercoaster ride in the industry that began with the great recession of 2008. From 2008-2009, the volume of industry shipments plummeted 8%, and the industry has been (slowly) crawling from the wreckage ever since. Currently, total volume of industry shipments is still slightly below the totals from 1995, a full two decades earlier.

On a positive note, the total volume of shipments was almost completely static between 2011-2013, so even the 1.2% increase must be met with some guarded optimism.

Another positive development comes in regards to the value of shipments, which increased to $30.5 billion. It’s only a .2% increase over the prior year’s shipments, but it continues an upward trend. In 2014, the value of industry shipments increased to $29.8 billion, up from 28.4 billion in 2013.

While volume and value of shipments inch higher annually, the breakdown of shipments delivered from corrugator plants (companies with their own corrugated production machines) vs. sheet plants (companies purchasing corrugated sheets from a corrugator plant, which they then convert) remain virtually unchanged. 80% of industry shipments in 2015 came from corrugator plants, while 20% came from sheet plants.

As the corrugated industry strives toward embracing sustainability in its operations, basis weights continue to trend downward. In 2015, the average basis weight of corrugated board was 131.4lbs per thousand sq ft, slightly lower than the 131.6lbs for thousand sq ft reported in 2014 and the 131.7lbs pounds for thousand sq ft in 2013.

Single-wall corrugated board remains dominant in the industry; in 2015, the board type accounted for 90.7% of all production.

Another report, this one from Research and Markets, forecasts the corrugated packaging market to grow at a CAGR of 4.6% during 2015-2020. A report from Technavio, forecasts the global corrugated box packaging market to grow at a CAGR of 4.8% through 2020, primarily as a result of the growth of e-commerce.

The growing e-commerce market, which primarily includes online shopping and was also pinpointed in the report from Persistence Market Research, has witnessed an increase in the demand for corrugated boxes for the shipment of products sold through them. The ease of online shopping has made many customers switch from the traditional method of shopping. Online retailers use different types of corrugated boxes, according to the product transported. The effective packaging is becoming one of the key business requirements in the e-commerce marketplace, thus fueling the growth of the market.

Sustainability

Environmentally conscious packaging, unsurprisingly, will continue to play a major role in how consumers interact with the products they purchase.

A recent study, “Global Green Packaging Market 2016-2020,” from Infiniti Research Ltd., predicts the global green packaging market will grow rapidly at a CAGR of more than 7% during the forecast period. Consumer demand for eco-friendly and sustainable packaging materials is on the rise, according to the study; hence, vendors are largely focusing on developing materials that can be recycled and have the traditional capabilities of resistance to friction, moisture, and heat.

The global green packaging market is well-diversified across Europe, the Asia-Pacific region, North America and the rest of the world, with Europe leading the market with more than 31% in 2015. The leading countries in this region are Germany, the UK and Italy. The increased demand for recycled packaging and recycled plastic products is the primary reason leading to the growth of the green packaging market in Europe.

In 2015, the recyclable packaging segment accounted for a significant share of over 76% in the global green packaging market. Recycling packaging material is gaining popularity among consumers because of the benefits they provide, such as reduced carbon footprint and energy conservation.

With a share of more than 54% in 2015, the food packaging market led the global green packaging market. The majority of the vendors in the market tend to use more green packaging materials to package food products.

Two thirds of American consumers (even higher among younger demographics) state that environmentally friendly packaging is a major factor in their purchasing decision-making, according to a new report from Mintel called “Global Packaging Trends.” Mintel points out that when product price and perceived product quality are equal, a package’s (and brand’s) environmental benefits will likely be the deciding factor for consumers.

Anti-counterfeiting

Sustainability may still monopolize much of the discussion in the packaging markets, but there remains one key issue that will continue to grow in importance: anti-counterfeiting.

Counterfeit goods pose serious threats to consumer welfare, as well as the brand loyalty of many CPG companies. The success of CPGs hinges on nothing greater than its ability to control the quality of its products. It is very difficult to gain goodwill among consumers. And once that goodwill is jeopardized, it is even more daunting a challenge to regain it.

Several reports suggest that the anti-counterfeiting packaging markets will continue to grow by enormous margins, as CPGs and retailers struggle to bring this epidemic under control. The anti-counterfeit packaging market size is projected to grow from $82.05 billion in 2015 to reach $153.95 billion by 2020, at an estimated Compound Annual Growth Rate of 13.41%, according to a new report from MarketsandMarkets.

The pharmaceuticals and healthcare sector is projected to be the fastest growing end-use sector in the next five years. Due to stringent laws and regulations enacted by the government and increasing importance given to package security by manufacturers, the demand for anti-counterfeit packaging technologies is projected to grow in this sector.

North America held the largest share in the anti-counterfeit packaging market and is projected to dominate the market during the forecast period, whereas, the market for Asia-Pacific is projected to grow at the highest CAGR. The rise in counterfeit products present in the market; increasing brand awareness; awareness among buyers about product information; the growing e-commerce industry; developments in printing technologies; and concerns regarding the impact of counterfeit products on the brand image of genuine product are all driving the anti-counterfeit packaging market.

Greg Kishbaugh, editor, Flexo Market News

Flexible Plastic Packaging 2016

Executive Summary

- Stand-up pouches are the fastest growing segment of flexible packaging with growth pegged at 7% per year to 2020.

- Digital printing for flexible packaging is becoming mainstream, with at least one significant converter, Bemis, announcing its intentions.

- Transparency, in every sense of the word, supports the growth of flexible packaging.

- Dynamic new packaging styles that take advantage of most or all of the benefits of flexible packaging are finally starting to assert themselves.

- Resin prices, already near or at historic lows, will likely continue to remain weak through early 2017.

Overview

The global flexible packaging industry enjoyed yet another strong year in 2016, with a sales growth rate once again significantly higher than U.S. GDP. All segments of the flexible packaging industry took part in this growth, but growth for value-added flexible packaging was even higher. Even under relatively flat or declining raw material prices, the industry revenues in 2016 grew at a healthy 4.6%. The growth in revenues for pouches grew at an estimated 7.6%.

At the recent Global Pouch Forum, Jörg Schönwald of Schönwald Consultinghs put the annual growth for stand-up pouches (SUPs) at 7% globally. Schönwald indicated that global demand for SUPs for liquid foods and beverages is approximately 165 million containers, a figure that represents less than 50% that of beverage cans, but is nevertheless an astonishing number when considering how few SUPs for liquids existed just a few years ago. Additionally, flexible packaging growth is stronger in developing countries than in the developed world, as can be seen from the chart below, again provided by Schönwald Consulting. The Asia-Pacific region accounts for more than 50% of all flexible packaging unit sales, while the Western cultures in Europe and North America account for only about 32% in total. Clearly, flexible packaging is a truly global industry.

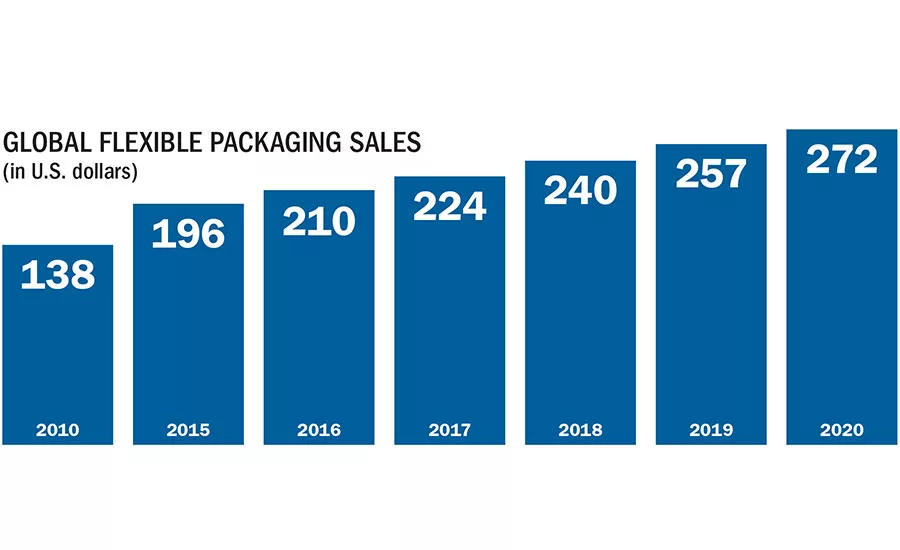

In the broader world of flexible packaging, the figures are just as impressive. Global flexible packaging accounted for approximately $210 billion in sales in 2016, with expected growth to at least $270 billion by 2020, according to multiple industry reports. These reports further indicate that flexible packaging (consumer and industrial) now accounts for more than 25% of the total global packaging industry, a share that continues to increase, primarily at the expense of rigid, non-plastic packaging. Industry reports again estimate the total consumer market for flexible packaging at more than $100 billion in 2016, which is projected to grow to about $145 billion by 2020. The industrial flexible packaging market segment is currently larger, at $110 billion, but not growing as fast as the consumer market and is much less profitable. Industrial packaging includes base engineered films, converting films, stretch and shrink films, roll wraps, overwrap, and all types of generic bags and other flexible packages. The growth rates indicate that developing economies will account for the greatest opportunities, with Asia leading the way, followed closely by Latin America.

Why the Pouch?

During the keynote presentation by Andy Gordon of The Campbell Soup Company at the 2016 Global Pouch Forum in Miami, FL, Gordon asked a critical question with the slide titled, “Why the pouch?” He was asking this for his company and the consumers they serve. The points he made to answer the question:

Convenient

- Easy opening (e.g. tear notch, laser perforation)

- Convenient to handle (e.g. zipper, shapes)

- Lightweight

- Reclosable

- Microwaveable

Fresher perception

- Preservation of flavor, texture, mineral and vitamins

- Extended shelflife

- Product visibility

Campbell’s is clearly one of the shining examples of a large CPG taking advantage of the benefits of flexible packaging, using the pouch to hold products as diverse as soup and cookies, frozen bread, to baby food to baby carrots. Campbell’s pouches include many of the key features available in this format, as well. Those include zippers, fitments, high-barrier clear films, retort pouches, laser-scored reseals, tactile films and hanging pegholes.

Packaging of any type needs to do the three Ps, as a minimum—protect, promote, preserve. When flexible packaging was first introduced to the consumer in the late 1940s, it was used only as a means of protection, meaning plastic bags were used to carry vegetables or maybe bread. Printing of plastic films developed slowly, so promotion was very limited. As for preservation, polymer science was limited to relatively simple versions of polyethylene (PE) in the early days, so some moisture protection was the best to be hoped for.

The development of even higher barrier films expanded dramatically after the introduction of biaxially oriented polyethylene terephthalate (PET) and polypropylene (PP) and, later, polyamide (PA) films. Vacuum-deposition techniques provided barrier protection and graphically appealing designs, and coextrusion and lamination techniques have revolutionized the industry. Thin-gauge barrier films with very high-end graphics and tremendous structural integrity are the norm in the industry today, but the truth is these techniques are really in their infancy, with much more development to come. In addition, polymer science has advanced exponentially, providing films with more toughness, rigidity, suppleness, flexibility, impact resistance and formability than ever thought possible. The ability of the current suppliers to print films with photographic quality on even the simplest structures is practically amazing. The barriers achieved with clear films have virtually matched foil in oxygen barrier properties and provide an even more robust package because of the pinhole challenges when folding thin-gauge foils.

Flexible packaging market growth has been driven by the replacement of traditional pack types—primarily metal cans, glass, plastic bottles and paperboard cartons across a wide range of end-use sectors. Flexible packaging has also benefited from a wider range of new products being developed by brand owners in an increasingly competitive consumer marketplace.

Barrier flexible packaging will continue to grow in importance as the consumer products goods makers (CPGs) major retail chains demand greater product protection and longer shelflife. Certainly, flexible packaging offers many of the benefits sought by brand companies and consumers alike. The graphical appeal of the print, along with new and unique shapes, sizes and decorative options, are unmatched in other packaging formats. These features, combined with many additional benefits inherent to flexible packaging but more challenging in others, will continue to provide the expected growth in this industry.

Sustainability

The light-weightedness of flexible packaging continues to contribute to the rapid growth of this package format, especially at the expense of rigid glass and metal packaging. The commercial success of baby food in pouches is well-documented, primarily due to the convenience of a self-serve pouch, plus the graphical appeal of the product on the shelf. However, the sustainable benefits of flexible in this market are not as publicized. According to information provided by the Flexible Packaging Association (FPA), empty pouches are 26 times less bulky to transport and store than unfilled glass jars, and up to 45 times lighter, even when comparing the same net weight per package. Comparing pouches for beverages against either plastic bottles or aluminum cans indicates similar carbon footprint reduction. Pouches consume somewhere between 0.54 and 2.90 fewer megajoules of energy per typical container size when compared to these rigid packages. Further evidence reveals that the package weight as a percentage of product weight is almost always an advantage of flexible. In addition, Earth’s Best branded baby foods, as well as CapriSun® and Honest Kids® pouched drinks, are now being collected through local TerraCycle® collection programs as a means to reduce solid waste in schools and other locations where children’s packaging is widely used. A number of other brands have joined TerraCycle’s efforts in the past few years. Recycling of flexible packaging is here to stay.

Printing

The big news in printing of flexible packaging in 2016 was the mainstreaming of digital printing as a viable commercial option vs. traditional methods. However, digital printing has begun to establish itself, due to its short-run capabilities, which opens up opportunities not only for targeted marketing approaches, but even customized packaging.

Sean Smyth from Smithers Pira highlighted this trend in his presentation at the 2016 Global Pouch Forum. Smyth highlighted the opportunity for digital printing in flexible packaging by identifying the key drivers:

- Low-cost shorter runs

- Prototyping

- Brand fragmentation

- Micro brands

- Rapid turnaround

- Versioning

- Personalization engagement

- New functionality

- Simplify supply chains

However, it is important to note the Smyth’s presentation also made a case for the converters to look beyond just digital printing as the answer to shorter runs and quicker turnarounds by considering the full supply chain in flexible packaging, including the materials used, color/brand management, convertibility of the desired final package, as well as food safety and other supply chain considerations. The converters who can seamlessly manage this process will become very successful in the years to come.

New flexible packaging. Clearly (pardon the pun) flexible packaging is on a roll. The CPGs have finally begun to use flexible packaging to highlight their products, rather than hide them behind opaque metal cans or full-sleeve bottle labels. The most obvious example of this trend was Happy Family’s introduction of Clearly Crafted brand of organic baby food in a clear pouch, the first such product in the increasingly crowded pouched baby food space. Happy Family made this launch with a “goodness you can see” tagline obviously intended to showcase their premium products. This trend towards transparency is taking shape across all food types, and flexible packaging plays a substantial role in supporting that. Transparency is much more than just a clear film on the pouch, however. Transparency is also about food safety, food quality, full life-cycle sustainability and “cleaner” labels. As noted by Gordon, fresher perception is a benefit of flexible packaging and the brand companies are using pouches to support that perception.

Food processing techniques

As the growth of pouches for shelf-stable foods and beverages continues to grow very quickly, the expectations from the CPG companies to offer a wider variety of products has opened up opportunities for new food processing techniques. The large CPG food companies, working with universities, co-packers, and food processing equipment companies, are starting to take advantage of the inherent adaptability of flexible packaging to a variety of processing techniques. It is very important to note that flexible packaging is the only packaging format that can be utilized with very few limitations across the board in all traditional and non-traditional food processes, including hot-fill, retort, aseptic, high-pressure processing (HPP), microwave-assisted thermal sterilization (MATS) and all combinations of these technologies.

2016 saw the launch of HPP baby food in a pouch, retort pouches for a much broader range of foods than before, plus the introduction of HPP large-format SUPs with a tap for multiple dispenses of juices. This pouch was launched in late 2016 by RIPE Craft Juice, New Haven, CT, into a pouch produced by Fres-co System, Telford, PA. The pouch is 1.5 liters and is sized to fit into a refrigerator for ease of use. Expect to see new pouches launched in 2017 that incorporate developing retort technologies as well, including continuous processors and MATS formats. The higher product density and much lower packaging-to-product ratios offered by flexible packaging will continue to provide opportunities.

Raw materials

It was another volatile year for resin and film pricing, although one that did not play out as clearly as one would expect. The price of natural gas in particular had a downward pull on resin prices, plus additional polymer capacity added to the downturn in pricing. The flexible packaging converting industry felt significant pressure to reduce their pricing as the CPGs saw commodity pricing trending down, and the industry had no choice but to follow the leaders. Barring a significant world event, resin pricing will likely remain near historic lows (based on constant dollars), through at least mid-2017, which will continue to depress pricing and challenge the flexible packaging industry to maintain their margins. The bigger challenge will come when resin pricing stabilizes and begins to increase again, creating huge pressures on cost-savings initiatives.

Industry Players

No discussion of the flexible packaging market in 2016 can be complete without an overview of the ongoing consolidation of this industry. The M&A activity continued very much apace, with some clear synergistic movements, along with the ongoing push by private equity in this segment.

Perhaps the biggest non-surprise of 2016 was Sealed Air’s announced spin-off of their Diversey Care division. The Diversey Care and Sealed Air’s legacy protective and food packaging businesses never enjoyed the expected synergies when the deal was announced in 2011. This divestiture should allow Sealed Air to refocus their packaging businesses and retain the strong positions they have maintained in the markets they serve. The transaction should be complete by Q3 2017.

The synergistic changes included strategic acquisitions as well as announced expansions. Sonoco acquired Plastics Packaging Inc., Hickory, NC, which will expand Sonoco’s short-run converting capabilities as well as move them into markets they do not currently serve. Also, Outlook Group, Neenah, WI, has merged with M&Q Packaging, Schuylkill Haven, PA – creating a formidable force in the combination. Canada’s TC Transcontinental has also been active, adding Canadian converter Flexstar Packaging, Richmond, BC to previous acquisitions Robbie Manufacturing and UltraFlex Packaging.

In addition, American Packaging Corporation (APC) announced a significant expansion of its rotogravure printing capabilities through a new facility in Wisconsin. This new capacity will firmly solidify APC’s position as the largest US provider of roto printing, and it comes on top of their recent expansion of their Story City, IA, plant. Also, Plastics Packaging Technologies, Kansas City, KS, completed the expansions and modernizations of their Kansas and Ohio facilities.

On the emerging technologies side, Bemis Company has installed an Indigo 20000 digital press from HP to support the growth in short-run and customized packaging. Expect similar announcements in 2017 as CPGs continue to expand this customization of their packaging.

Private equity continued to play an active role in the flexible packaging market in 2016. Wellspring Capital complemented their consolidation of Coating Excellence International and Prolamina into Ampac, creating ProAmpac, a substantial force in the converted flexible packaging market. Wellspring also acquired Vitex Packaging Group, Suffolk, VA to support their paper converting business. Wellspring then sold the combined companies to Pritzker Group, Chicago, IL. Pritzker has made it clear that they believe further consolidation is necessary in this industry, and they intend to be a force in that movement.

The ongoing saga that is the merger of Dow Chemical and Dupont will drag into mid-2017, at least. There has been significant legal disruption in both North America and Europe over regulatory and antitrust issues, primarily with agricultural chemicals, but also with some of Dow’s copolymer businesses. These issues have mostly been resolved in the U.S., but they remain in Europe and will likely not be resolved until mid-year or so. In the interim, the companies have begun the process of combining businesses, and significant downsizing should be announced when the merger is completed.

Danny Beard, president, Packaging Specialists, dabeard@sbcglobal.net

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!