Special Report: Performance Review

Mixed Year Financially for U.S. Packaging Companies

Charles Gross is an analyst with Morningstar

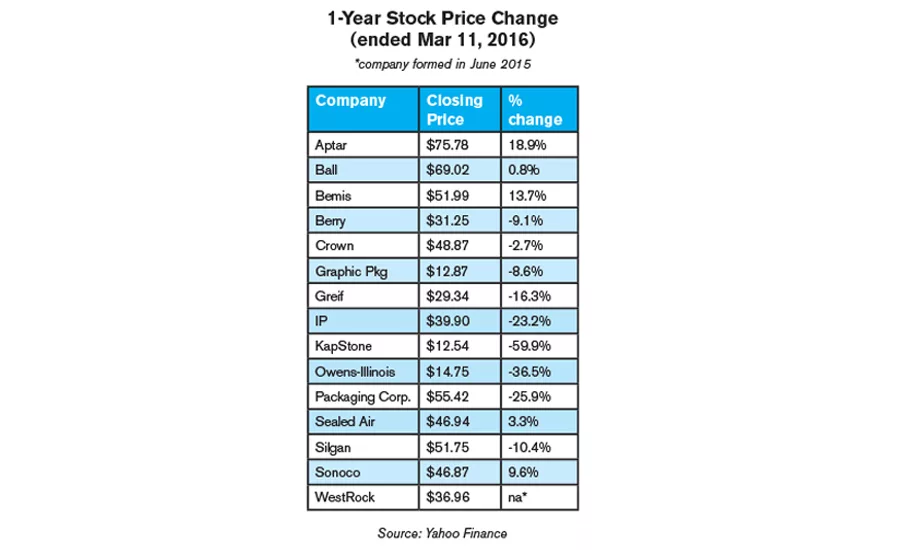

Stock price changes for packaging companies ranged from -59.9% to 18.9%.

While their prospects may not be as bright, two of the paper packagers—International Paper Co. and WestRock Co.—didn’t do badly in 2015.

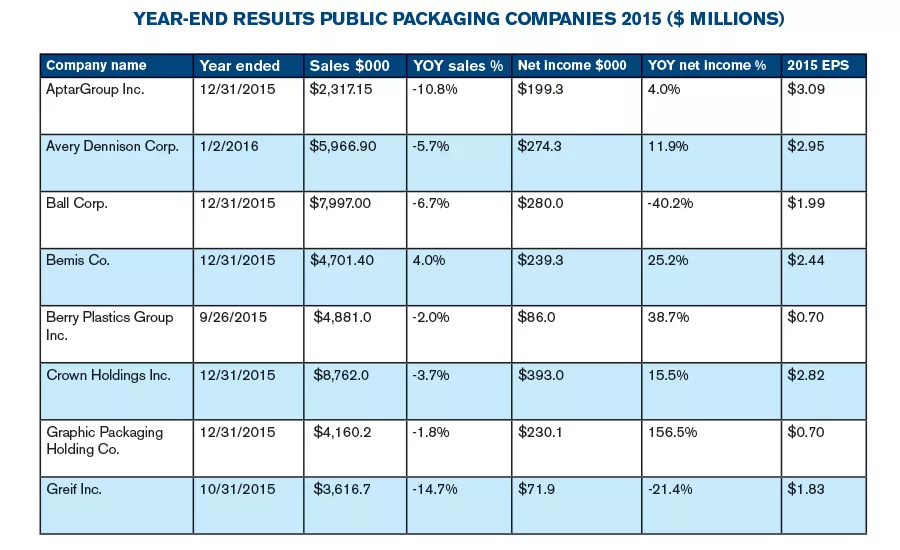

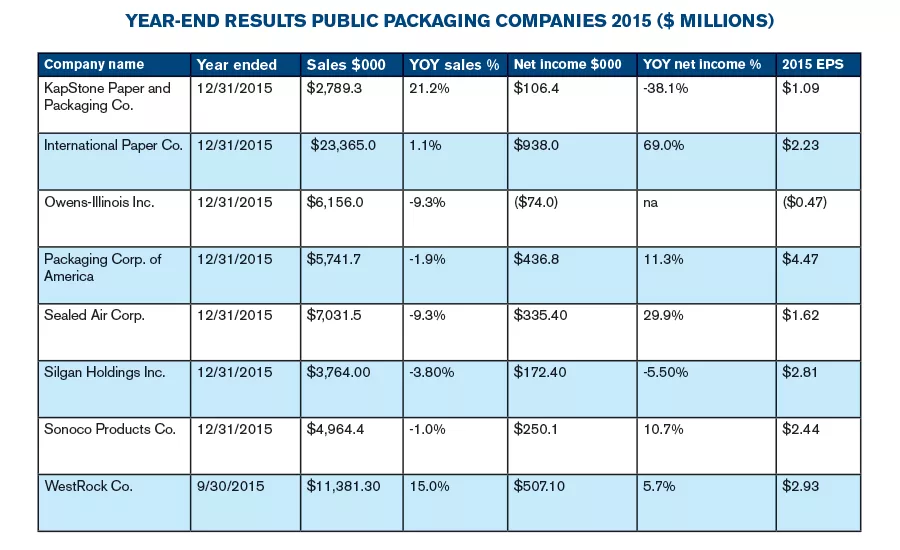

The 2015 year-end results for public packaging companies, in millions, in alphabetical order.

CONTINUED: The 2015 year-end results for public packaging companies, in millions, in alphabetical order.

The stronger dollar battered 2015 revenue for publicly held U.S. packaging companies. In Packaging Strategies News’ analysis of the 16 in our group, sales growth averaged only 1.8% for the year.

The bright spots were among plastic packagers with exposure to the pharmaceutical markets, which outperformed the paper packaging companies. “Indeed the plastic packagers has some of the best fourth-quarter results thanks to lower resin costs, while the containerboard producers had difficult quarters,” wrote KeyBanc Capital Markets analyst Adam Josephson in a research note.

Many packagers have extensive overseas manufacturing operations and exports to serve growing consumer markets and rising middle classes. But even though sales volumes may be growing there—for instance Sealed Air had growth exceeding 6% in Latin America—they look smaller when converted back into dollars.

Currency translation effects also sliced profit at many companies, as they have with American corporations in most every industry. That is putting renewed emphasis on cost-cutting and putting the brakes on some capital spending.

The positives

Featured Packaging Companies

AptarGroup | Avery Dennison | Ball | Bemis | Berry Plastics | Crown Holdings | Graphic Packaging Holding | Greif | International Paper | KapStone Paper and Packaging | Owens-Illinois | Packaging Corp. of America | Sealed Air | Sonoco | WestRock

Some of the best performers were at the top of the list alphabetically (see chart above). AptarGroup Inc., despite lower revenue, had record profit. Reported earnings per share rose 8% year-over-year and adjusted EPS was up 21%. Operating margins across each business segment were improved.

The company had a particularly strong year in its pharma segment, with sales growth topping 8% in 2015. Analysts are bullish growth prospects for its dispensing products.

Avery Dennison Corp. also had a strong 2015, making progress in both of its major segments, pressure-sensitive materials (PSM) and retail branding and information solutions (RBIS). Net income was up almost 12%.

“We continue to highlight Avery as our preferred stock in the group given its favorable fundamentals, strong balance sheet and elative discount to the other plastic packagers,” Josephson said.

While their prospects may not be as bright, two of the paper packagers—International Paper Co. and WestRock Co.—didn’t do badly in 2015. Producers were dealing with a weakness in containerboard prices, capacity additions and excess inventory, and rising raw material costs for recycled fiber. And corrugated packaging isn’t a growth business.

So how did they do it? Producers took “economic” downtime throughout the year as export pricing weakened. They also were aggressive on pricing.

Will this continue into 2016? While the industry is expected to remain focused on balancing supply and demand (both IP and WestRock are taking out some capacity this year), increased competition could diminish profitability. “We expect to see…reduced margins as domestic price competition heats up,” wrote Morningstar analyst Charles Gross in a February report on IP. And more mill conversions to board from paper could add to the situation.

In IP’s favor is that the majority of its consumer packaging business is food and beverage, which is less volatile than others. E-commerce should help box demand, but the outlook is generally subdued: The RISI forecast for U.S. corrugated packaging market growth for 2015-2019 is only 1.8% year.

Here is a look at the players in more detail.

AptarGroup Inc. (NYSE: ATR)

Aptar turned in a strong 2015, with earnings per share up 8%. Operating profit rose to $324mn from $306mn in 2014. Overall sales fell, hurt by currency exchange differences. Operating margins improved in all business segments, especially pharmaceuticals where core sales were up 6% year-over-year and EBIT margins expanded to 28.7%.

The pharmaceutical division, which accounts for 30% of net sales, is a big earner, accounting for about 60% of total operating profit. Morningstar analyst Daniel Rohr on Feb. 28 said that he expects the pharma segment to be the fastest-growing at around 7.5% annually “as baby boomers continue to age and the risk of respiratory illness increases.”

In a call with analysts, CEO Steven Hagge said that the company continues to expand its product portfolio. “Our airless serum dropper, originally developed for the skin market, is now featured on a new luxury hair serum product in Europe.” In the pharma segment he said a nasal spray pump used for allergy medications will go over-the-counter with the Rhinocort brand, which had previously been prescription-only. The Aptar nasal spray pump is also used with the first FDA-approved, ready-to-use needle free nasal spray for Narcan, which can stop opioid overdoses.

Avery Dennison Corp. (NYSE: AVY)

Avery Dennison reported fiscal 2015 sales fell 5.7% to $5.97bn, while net income rose 11.9% to $274.3mn. Reported sales were down for the fiscal year in both the PSM and RBIS divisions, 6% and 4%, respectively, although they were up if adjusted for acquisitions and divestitures and currency translation. Overall, if taking those items into account (called organic growth) total company sales rose 4.6%.

CEO Dean Scarborough said on the PSM side, the company is investing in capacity for graphics manufacturing. “We’re adding coding capacity in Asia to support still-solid growth in that regional and we are investing in information systems to drive supply chain productivity by upgrading systems in our North American materials business,” he said in the analyst call.

In RBIS, he said the forecast is for the unit to grow 15%-20% a year through 2018. “Sales of RFID products increased by more than 20% this year, and we expect that momentum to continue through 2016,” he said.

He added he expected to “accelerate growth” in the Vancive medical technologies business ($72.9mn or 1% of sales in 2015) this year “while delivering continued margin expansion.” Vancive makes adhesive products for films, patches, and tapes.

Ball Corp. (NYSE: BLL)

Ball reported full-year 2015 net earnings of $280.0mn (or $1.99/share) on sales of $7.99bn compared with $470.0mn, or $3.30/share on sales of $8.57bn in 2014. Earnings were unfavorably impacted by foreign currency exchange, start-up costs and other one-time costs. In addition, the company said a shift away from metal cans by some food brands impacted sales in the North America, which were partially offset by strong performance in aerosols. During the fourth quarter, the company completed investments in Europe and India to meet the strong demand for metal spray cans.

Profit in metal beverage cans in the Americas and Asia was down slightly (operating earnings of $510.9mn in 2015 vs. $534.8mn in 2014), affected in part by start-up costs for a new can and end line in Monterrey, Mexico, and an excess of industry capacity in China, and continued price erosion there. A new beverage can plant in Myanmar is expected to open in April; a second can line will start up in midyear in China.

“While our biggest challenge is to weather the unsustainable pricing environment in our China beverage can business, overall we feel good about where we are,” said CEO John Hayes in a conference call with analysts.

Hayes said the pending acquisition of Rexam PLC will likely close in the second quarter.

Bemis Co. (NYSE: BMS)

The flexible packaging maker earned $239.3mn, or $2.44/share, in 2015 on sales of $4.07bn. That compared with net income of $191.1mn, or $1.89/share, in 2014. Full-year 2015 adjusted diluted EPS from continuing operations were $2.55, up 10.9% compared to the prior year.

The company is targeting revenue of $5.8bn in 2019, and is focusing on investing in high-barrier film development for the meat, cheese and dairy end markets.

Bemis has good positions globally with growing businesses and the year-end report showed the company is pointed in the right direction. However, sales of $1.32bn in the Global Packaging division were down 10.7% compared with 2014, due to foreign currency effects, primarily in Latin America, where it as significant holdings.

The company said 15% of revenue was from new products created over the past three years. Bill Austen, president and CEO, said in a call with analysts that the company’s product development center in Neenah, WI, has been popular with customers. ”We’ve had close to probably 100 ideation sessions thus far and we’re driving new ideas and new thoughts for different types of packaging out of that location.”

Berry Plastics Co. (NYSE: BERY)

Net sales for the 2015 fiscal year were $4.88bn compared with $4.96bn in fiscal 2014. The decrease was attributed to lower selling prices due to the pass through of lower raw materials costs. (Resin accounts for about 50% of cost of goods sold.) Net income rose to $86.0mn.

The results included the Avintiv business acquired last fall. That puts Berry in the nonwovens industry, making materials used in diapers, wipes, hospital gowns, and feminine care “We remain excited about the acquisitions and the benefits that we believe the combination of the business will generate,” CEO Jonathan Rich said in call with analysts.

Berry is integrating Avintiv into a new Health, Hygiene and Specialties division which also includes flexible personal care and medical products. It represents about 35% of sales. Rich said he expects 2% sales growth in fiscal 2016.

The new Consumer Packaging Division includes the former open and closed top segments, flexible packaging for food and consumer products, and shrink film. That is about 45% of sales. This year, growth is expected to be about even with 2015. The third division is Engineered Materials, which includes converter films, tapes, can liners, and bags.

Mark Miles, CFO, also said that the recyclable polypropylene Versalite cup that is being trialed by Dunkin’ Donuts has had “growing pains” due to oil prices dropping. “The cost difference between the expanded polystyrene and either paper cups or Versalite cup alternatives has widened,” Miles said. Versalite is marketed as a greener than polystyrene foam. He said customers continue to switch from Styrofoam, “but the cost penalty they have to incur has widened,” which will have an impact on how fast sales grow.

Berry has had success winning Frito-Lay as a customer for its container, closure, seal combination from its NuSeal and Barricade lines. NuSeal is made from a film that is optimized for barrier and temperature requirements.

Crown Holdings Inc. (NYSE: CCK)

Crown delivered sold 2015 results as higher margins offset weaker volumes. Profit in its two largest segments—Americas beverage and European food—improved because of the acquisitions of Empaque and Mivisa.

Global beverage can shipments increased 9% in 2015, including Empaque. In 2016, the company will build three new beverage can plants: in Nichols, NY, which will make specialty sizes; and beer can facilities in Phnom Penh, Cambodia, and Monterrey, Mexico. Additionally it is doubling production capacity at the Rossmoyne, Turkey, plant by adding a second production line to be operational in the fourth quarter.

For 2015, net sales were $8.76bn, compared with $9.07bn in 2014. Net income rose to $393mn, or $2.82/share, from $387mn, $2.79/share, the previous year.

The company said beverage can volumes rose 8% in Asia Pacific, and that strong performances throughout Southeast Asia offset continuing challenges in China.

While beverage cans did well, the company closed four food can and end factories—two in North America and two in Europe—and sold five European specialty packaging facilities. North American food can sales were down 16%.

President Tim Donohue said in a conference call with analysts that the company has been capacity-constrained at times to produce the popular 12oz can. “I think the future should be very bright in North America as we continue to take on the challenge of declining carbonated consumption but replace it with coffees, teas, energy drinks, et cetera,” he said.

Graphic Packaging Holding Co. (NYSE: GPK)

Full-year net income was $230.1mn, or $0.70/share compared with 2014 net income of $89.7mn, or $0.27/share. When adjusting for a loss of the sale of assets in 2014, charges, and taxes, income was $247.0mn in 2015 versus $238.1mn in 2014.

Net sales decreased 1.8% to $4.16bn, from $4.24bn in 2014. The decrease was driven by lower sales due to divestitures, unfavorable foreign exchange rates, and lower pricing. That was partially offset by improved volumes from acquisitions.

The company last year bought Carded Graphics, and Walter G. Anderson in the U.S. plus Colorpak in Australia and G-Box in Mexico.

CEO Michael Doss said in a statement: “Investing in high-return projects and strategic acquisitions remains a core part of our profitable growth strategy.”

Greif Inc. (NYSE: GEF)

Greif reported lower sales and lower profit for fiscal 2015. However, after adjusting for currency and divestments, sales were flat.

Operating profit of $192.8mn included $15.0mn for asset impairment for the company’s Venezuelan property.

During the year, two underperforming operations were closed in Turkey and Morocco, landholdings were sold in Canada, and manufacturing facilities in Germany, Houston, and Missouri, were consolidated to save costs.

With the rigid Industrial market sufficiently consolidated, Greif’s focus has shifted to acquisitions in the industrial flexible product market. However, sales and earnings in that segment were below expectations. This year, the company could be impacted by raw material price hikes, such as steel and recycled materials for containerboard.

International Paper Co. (NYSE: IP)

International Paper reported 2015 net earnings of $938mn ($2.23/share) compared with $555mn ($1.29/share) in full-year 2014. Annual net sales totaled $22.4bn compared with $23.6bn in 2014.

In looking at segment profitability, EBITDA was good—up 22%— in industrial packaging, but the Brazil operation was down more than 17%. IP has four box plants and three containerboard mills there and sells most of what it makes in the country. CEO Mark Sutton said in a call with analysts that Brazil is in a “pretty significant recession… It doesn’t have a large export… We use everything we make.” He said the business is “a bit of challenge. So we’re just trying to stabilize, make sure we have the right customers.”

Elsewhere, IP is a big player in export markets, which were volatile in the second half of last year. Timothy Nicholls, senior VP for industrial packaging, said demand was weaker in the Middle East, particularly Turkey, due to political conflict, “But on balance demand has held up fairly well. And we continue to see that in the first quarter.”

Regarding the overall box business, executives said the market could grow upwards of 1% in the first quarter.

KapStone Paper and Packaging Corp. (NYSE: KS)

KapStone reported a drop of 38% in net income for 2015. CEO Roger W. Stone said in a statement that the year was a challenging one, “Including the impact of a stronger U.S. dollar resulting in lower export containerboard and extensible grade paper prices with increased competition in certain export markets.”

Shutdowns also contributed to a loss of tonnage produced and profits in the fourth quarter. Also in the quarter, executives said the export market for kraft paper was poor and the strong dollar led to competitors offering aggressive pricing.

Exports account for about 20% or revenue; export product revenue fell $37mn in 2015, they said in an analyst call, and average selling prices were down about $40/ton. During the year, prices for virgin fiber were higher.

Consolidated net sales for the year were $2.79bn, an increase of 21.2%, compared with 2014 sales of $2.30bn. The increase was primarily due to the June acquisition of Victory Packaging, partially offset by lower volume and selling prices and a stronger U.S. dollar.

Owens-Illinois Inc. (NYSE: OI)

For full-year 2015, the glassmaker recorded a loss from continuing operations of $0.44/share on revenue of $6.16bn. Excluding items including a charge for asbestos-related costs, adjusted earnings were $2.00/share.

While overall sales dropped about 9%, volumes were up 3% over 2014, the company said. Adverse currency exchange due to the stronger U.S. dollar accounted for the sales decline. Excluding the acquisition of Vitro’s food and beverage business, volumes were on par with the previous year.

On a global basis, volumes of wine, spirits, food and non-alcoholic beverages all grew year-on-year. While global beer volumes fell 1%, driven by a decline in mainstream beer, shipments into craft and premium beer continued to expand.

“Looking ahead, we expect that trends in the majority of our end markets will remain stable in 2016 and O-I will increasingly benefit from our growing exposure to U.S. beer imports and the Mexican domestic market,” CEO Andres Lopez said in a statement. “While we recognize continued external uncertainties, such as economic conditions in Brazil and price dynamics in Europe, we are pressing hard on key initiatives that will increase profitability in 2016, including: maximizing the value of the acquired business; improving our end-to-end supply chain performance; and reducing costs through increasing organizational effectiveness and spending discipline. We expect to deliver higher earnings and cash flow in 2016 while continuing to prioritize deleveraging our balance sheet.”

Packaging Corp. of America (NYSE: PKG)

For the year, the company reported net income of $436.8mn, or $4.47/share compared with 2014 earnings of $392.6mn. Revenue was $5.74bn, down from $5.85bn. A rebuild of the Jackson, AL, mill impacted volume. Export prices were also lower in the fourth quarter.

Looking ahead, company executives said lower containerboard prices could impact earnings in the first quarter.

CEO Mark Kowlzan also said the company could be in the market for acquisitions, now that the integration of the Boise box assets is behind it.

Sealed Air Corp. (NYSE: SEE)

For full-year 2015, net sales totaled $7.03bn, a decrease of 9.3% from the previous year. The effect of currency translations had a negative impact on sales, as well as divestitures in the Food Care division. Without the currency effects, overall sales exclusive of divestitures rose 2.8%

In 2015, the company sold its North American and European food trays businesses. Reported sales in Food Care (films and bags) for the year were down 11%; in the Diversey division (cleaning supplies and equipment) down 8%; and in Product Care (secondary packaging) down 7%. Also impacting Food Care were lower beef sales.

Net income was $335.4mn, or $1.62/share, compared with $258.1mn, or $1.20/share in 2014.

In food packaging CEO Jerome Peribere said the company was awarded a Darfresh vacuum skin packaging contract for red meat, poultry, and seafood from a large Asia-Pacific supermarket chain, the first in the region.

In Diversey, the acquisition of Intellibot Robotics in March has moved it into the robotic floor care equipment market. Peribere said it has more than 200 machines operating today. Silgan Holdings Inc. (NASDAQ: SLGN)

Silgan reported full-year 2015 net income of $172.4mn, or $2.81/share, compared with 2014 net income of $182.4mn, or $2.86/share.

Net sales were $3.76bn, a decrease of $147.8mn, or 3.8%, compared with 2014. The decrease was due largely to the impact of unfavorable foreign currency translation and the pass through of lower raw material costs.

The plastic container business struggled in 2015, with sales down 9.9% and margins diving down to about 1%. “We believe EBIT margins will stabilize in 2017 as this segment is rebalanced,” wrote Morningstar analyst Daniel Rohr in a research note.

The company is building three new rigid container manufacturing plants to reduce costs. They are in North East, PA, Hazelwood, MO, and Burlington, IA. Plants that are reportedly being closed are located in Lodi, CA, LaPorte, IN, and Woodstock, IL.

The company could be an acquirer of some of the divested assets from the Ball/Rexam merger.

Sonoco Products Co. (NYSE: SON)

Net sales for 2015 were $4.96bn, down 1% compared with $5,02bn in 2014. Negative foreign currency translated reduced reported sales, as did lower selling prices, despite added sales from acquisitions.

The Consumer Packaging segment achieved record sales, up 8.1%, and operating profit was up 15.5%, due in part to the Weidenhammer acquisition. The flexible packaging business experienced sales growth of 9.8% and expanded operating profit of 21.7%, through market share expansion, price/cost management, and solid productivity improvements.

However, sales were down 9.1% in the Display and Packaging unit, primarily because of negative foreign currency translation; operating profit was flat year-over-year. Sales were down 9.1% in the Industrial segment as well with operating profit down 24.5%. In a conference call with analysts CEO Jack sanders said consolidations of plants in that unit was a possibility.

WestRock Co. (NYSE: WRK)

WestRock, which was created in July 2015 after the combination of RockTenn and MeadWestvaco, is seeking to cut costs out of the system and boost productivity. “We continue to have enthusiastic alignment across the company about our aspiration to be the global industry leader in consumer and corrugated packaging markets. We’re making significant strides in areas that are driving value from the merger, including the integration of our organizations, the realization of the merger-related synergies and performance improvements,”

The company announced closures of facilities in Tennessee and Ohio that make merchandising displays, and a paper mill in Uncasville, CT.

It also plans to spin off the former Mead specialty chemical business into a public company, which has been renamed Ingevity. The transition is expected to occur in May.

Paper Packaging Income Growth To Be Limited

Demand for paper packaging will continue to grow modestly over the next 12-18 months, a new report from Moody’s Investors Service says. However weaker prices across most grades of paper and forest products will limit operating earnings growth.

The firm rates the entire sector “stable” and that is the rating given to the paper packaging and tissue sub-sector as well. Paper packaging companies in North America and Europe are expected to generate flat to modestly stronger operating earnings (in the range of 0%-2%) in 2016.

That is a result of declining product prices caused by excess supply that entered the market in 2015. Partially offsetting will be cost-savings and synergies from acquisitions. Higher labor and recycled material costs could be offset by productivity improvements

Paper packaging accounts for about 40% of the U.S. packaging marketplace, which stood at $141.2bn in 2014, according to an estimate from the Freedonia Group. It slightly outranks plastic, which had a 39% share.

The paper packaging share is not expected to grow significantly, but won’t decline “primarily due to global economic growth and steady food and beverage consumption.” (Growth will be affected by consumers, manufacturers, and retailers moving to reduce the amount of packaging to transport, protect, and display products.)

Capacity

In North America, containerboard capacity additions this year are limited to less than 200,000 tons, the report said. “However the ramp-up of about 1mn tons of new capacity last year created an excess supply situation that led to linerboard and corrugated medium prices declining about 2% in early 2016,” Moody’s said.

It expects North American unbleached kraft linerboard prices to drop about 2% from 2015, and bleached kraft board to also be down 2%. Recycled folding boxboard will likely increase by 3%.

Producers are expected to take steps to take market downtime or close older, less efficient capacity to balance supply with demand this year.

Also affecting the market is the strong dollar, which makes U.S. exports less cost-competitive with supplies from Europe, Latin America, and Canada.

There is a huge amount of containerboard capacity coming on line this year in Europe and China. That is expected to mostly serve domestic and emerging markets, but imports could also affect prices here.

Morningstar: Stable Growth but Headwinds Ahead

Charles Gross is an analyst with Morningstar. He took over coverage of the paper and packaging industry last September. Packaging Strategies News caught up with him to talk about the public company financial performance in 2015.

What company do you think was the top performer in 2015 and why?

It’s kind of hard to say who is the star. All of the companies came under currency pressure; a lot of the companies had good strong underlying growth. In terms of underlying performance, Aptar came in with strong numbers as their pharmacy business grew. They had margins up to 30%, which is impressive considering all the headwinds.

What role did currency play as opposed to declining global economic growth?

A mix. The currency had real effect on revenue. [Otherwise] there were pockets of growth and pockets of decline, depending on the business of the packaging company. We had some slower numbers come from developed markets but emerging compensated for that.

Do you see the currency as a problem in 2016?

Currency is going to be moving around a lot going forward. We are likely to see more volatility.

What is your take on emerging markets?

Emerging markets still play a positive role. Obviously Brazil is still developing. China exposure is a relative negative trend. But we think Southeast Asia will be one of the shining stars in 2016. Latin America to a lesser extent, but it’s a mix picture. A number of companies there are dependent on oil revenue.

What role did lower resin prices play in the financials?

They ended up widening margins. [However] some companies had hedges in place, or passed [them] through in contracts. A lot didn’t have any huge price changes.

Do you think the specialized companies like Aptar do better than those with broader product offerings?

I think you get more volatility in specialized markets, depending on the specialization. Avery’s RBIS business is a little clumpy. With Aptar we are seeing really high growth, an interesting story with an aging population. With a company like Bemis, that sells to a more differentiated base, we see more cyclicality; if you’re selling food packaging, during the downturn customers may shift to cheaper products. There is a little bit of a different result depending on the business.

IP and WestRock didn’t do badly, but they are not in a growth segment. What’s next for them?

In our view, we don’t think that’s sustainable. Linerboard benchmark prices were down quite a bit last year and we saw a drop in domestic prices at the end of 2015. Consolidation has helped. But we think the biggest threat is conversion of paper machines to more profitable linerboard machines and that has the potential for capacity to outstrip demand.

Are you recommending any companies that could do well in 2016?

For the most part the companies on my list are fairly valued or overvalued. But one company that is still relatively undervalued is Crown. There is a lot of focus on Rexam and Ball and rightly slow. But the market has overlooked Crown a bit. We think organic growth rates and consumption of beer and soda will be strong in emerging markets.

What is your outlook for the packaging group in 2016?

For the most part our outlook is stable demand growth. There are going to be foreign exchange headwinds—or tailwinds—weighing on the results. I don’t think any huge changes are coming.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!