Four Drivers for Luxury Packaging Markets

The distinction between mass-market and luxury products is becoming blurred, prompting luxury brands to turn to innovative technologies and strategies to attract customers to their high-end goods.

According to the Smithers Pira (smitherspira.com) report, "The Future of Luxury Packaging to 2022," the luxury packaging market was valued at over $13.77 billion in 2016, with global sales forecast to increase by 3.4 percent in 2017 to $14.25 billion. In volume terms, a growth rate of 2.6 percent is forecast for 2017, after which the world market is expected to increase by an annual average of 1.3% up to 2022.

The major new study from Smithers Pira pinpoints the main developments in technology that are expected to aid market growth over the next five years. Among the four principal drivers are:

- Using packaging as a medium to premiumize a product

- Creating a consumer connection via personalised and customised print

- The growing importance of consumers in non-traditional markets

- Engaging with an online sales culture

Premiumization

Premiumization is a trend apparent in many sectors of the packaged goods industry. Brand owners are seeking to attract consumers by offering products positioned on an ‘everyday luxury’ platform, and packaging is seen as a way of achieving this.

The food and drink industry has been one of the main pioneers of the trend toward more premium forms of packaging. One successful example from the U.K. food industry is the Gü range of desserts, which is marketed on an indulgence platform and whose black-coloured packaging marks it out as a premium product.

Appearance and aesthetics are major factors when designing packaging in this sector and in others fast-moving consumer goods (FMCGs) industry. Considerable attention is paid to areas such as colour, images and graphics. Increasingly, brand owners are having to consider what packaging for their products looks like on screen as well as on the shelf, given the fact that more people are now purchasing goods via online channels.

Personalization and Customization

Digital printers in many parts of the world are increasingly benefiting from the recent growth in demand for personalized gift products, a trend that carries strong implications for the luxury packaging industry. Personalized printed products are now being offered by many leading brands, with consumption peaking during gifting occasions, like Christmas and Valentine’s Day. For example, the U.K. market for personalized gifts was valued at nearly $1.3 billion in 2015, with an average expenditure per consumer of almost $47.

Some more recent examples of this trend specifically within the luxury goods sector include:

Chocolate

Companies competing at the upper end of the chocolate confectionery market now offer personalized products and packaging, most of which are targeted at the gifting market. Thorntons now sells personalized chocolate boxes in the form of Alphabet Truffles, in which the chocolates can form messages, such as birthday wishes. Ireland-based firm Lily O’Brien’s offers consumers a choice of chocolate box packaging and the ability to upload photos or images to personalize the printed pack.

Premium alcoholic drinks

A number of premium brands, particularly within the Scotch whisky sector such as Glenfiddich, Glengoyne, Gordon & MacPhail, now offer personalized labels, mainly for gifting purposes with individual messages.

Jewelry

In this sector, personalized gift packaging is usually in the form of gift boxes or bags, although some companies have started to customize secondary packaging, such as tissue paper and ribbons. Keenpac’s jewellery boxes are created on a bespoke basis and come in a variety of shapes and sizes.

Ordering such gifts is increasingly easy for the consumer due to the proliferation of web-to-print ordering systems.

Coca-Cola’s Share a Coke campaigns featuring bottle labels carrying common individual forenames, remain the most well-known example of a major brand applying customization to create a more personal connection with its consumers. Coca-Cola has sold more than 150 million of its personalized bottles.

The print costs of such campaigns—using toner or increasingly inkjet presses—are declining, but remain significant. Luxury segments have and will continue to be a key area for this pioneering technology, as one that can accept the premium for such printing for special and seasonal editions more readily. The range of options available is now being supplemented by new printing equipment and finishing systems for new pack formats—like flexible pouches, and folding cartons—and high-grade substrates optimized for accepting digital print graphics.

Non-Western Growth Markets

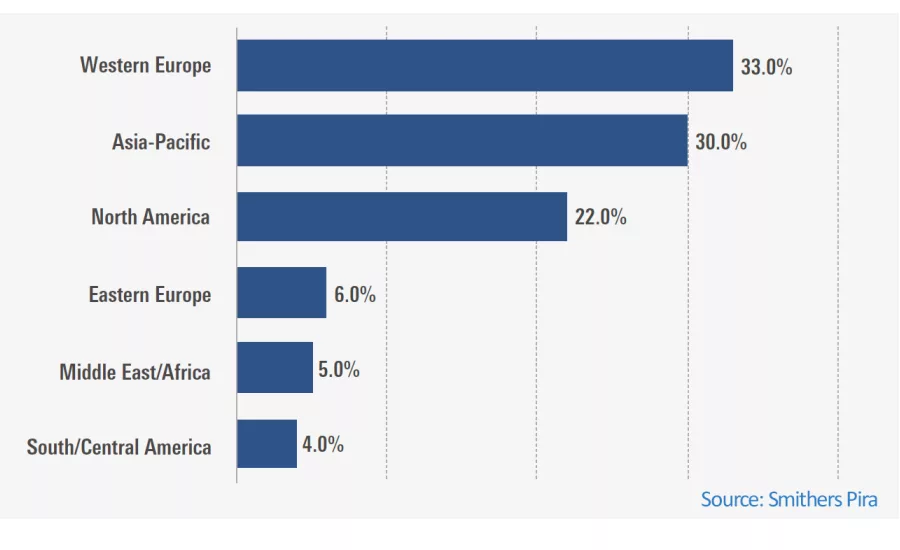

As the market for luxury goods has become more international, the leading brands have commanded a wider geographical footprint. From a supply perspective, the luxury goods market is highly concentrated. It is estimated that the larger European brands currently account for up to 70% of global sales, which gives some indication of their long-standing strength and heritage across much of the world.

Sales of luxury goods in non-western regions have benefited from factors such as the emergence of a more affluent urban consumer base and a greater number of youthful and Western-oriented consumers. Much of the growth in the global luxury goods market has come from China. According to recent analysis global luxury sales would have contracted by around 2 percent on average between 2012 and 2015, had it not been for Chinese consumers.

Shopping for luxury goods while travelling is an increasingly common activity for the emergent middle class in China and elsewhere, with airport malls a focus for this trade. Some research shows shoppers at airport malls accounted for 6 percent of total worldwide expenditure on luxury goods in 2016, up from 4 percent the previous year.

Online Sales and “Showrooming”

Online channels are making a greater impact within the world market for luxury goods. Online sales of luxury goods are set to reach almost $42 billion by the end of the current decade, up by more than 95% from levels observed in 2014.

The growing importance of the online sector has also contributed to the ‘showrooming’ trend, whereby consumers research products in-store, only to complete their purchases via online channels. This has been apparent in the luxury goods market, particularly since many of the world’s leading fashion houses have been relatively slow to adopt e-commerce. It was estimated in 2016 that up to 40% of luxury brands had little or no online sales capability. Consumers are becoming increasingly price conscious, and are therefore attracted to the special offers and discounts typically offered by online retailers.

In-store shopping is expected to remain a mainstay of the luxury goods market, since most consumers still want to touch, feel and smell products prior to purchase. Traditional retailers have already responded to the growth of the online/mobile sector via tactics usually referred to as ‘reverse showrooming’ - sometimes called ‘web-rooming’ - whereby consumers research products online, and then complete their purchases in-store. The increasing popularity of ‘unboxing’ videos on social media is also putting a new focus on materials and design, with ‘experience’ packaging making this process part of the overall enjoyment of the product.

There has been a growth in Click & Collect schemes within the industry, with retailers offering improved convenience and knowledgeable staff to entice consumers. The coming years are therefore likely to see retailers of luxury goods operating across multichannel platforms, combining in-store, online and mobile purchase points.

These four trends are examined, analysed and quantified in greater depth in the Smithers Pira report. Other major topics explored include:

- The growing need for anti-counterfeiting and brand protection

- Wider use of intelligent and interactive packaging

- Greater availability of haptic effects to give packaging a luxury feel

- Brand owner and consumer desire prompting the development of new sustainable and/or environmentally preferable packaging materials.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!